Pensions and allowances are adjusted annually with a view to protecting beneficiaries’ purchasing power and taking into account the financial balance of the Fund.

A purchasing power loss mechanism is in place such that an annual adjustment is not granted or is slowed down until individual beneficiaries have accumulated a purchasing power loss of 8%. Thereafter Geneva Cost of Living (CVI) is granted.

There are different methods for calculating the annual adjustment and these are described inAnnex C of the Fund’s Rules. The applicable method depends on your personal situation and particular dates. To determine which method is relevant, please refer to the following guidance:

If you are a beneficiary of a retirement or total disability pension, the date that you became a beneficiary corresponds to your pension start date.

If you are a beneficiary of a surviving spouse’s pension or an orphan’s pension, the relevant date is the date when the deceased beneficiary became a beneficiary.

If you are a beneficiary of a retirement pension having participated in the Progressive Retirement Program (PRP), the date you became a beneficiary corresponds to your PRP start date.

If you are a beneficiary of a surviving spouse’s pension or an orphan’s pension following the death of a member, the relevant date is your pension start date.

Should your date be:

on or before 31 December 2011, the applicable method would be I. 1. of Annex C.

between 1 January 2012 and 31 July 2019 the applicable method would be I. 2. of Annex C.

on or after 1 August 2019, the applicable method would be I. 3. of Annex C.

Each year, as a beneficiary, you receive a letter with details of your annual adjustment and individual PPL account balance.

How do I know which method in Annex C of the Rules applies to my situation?

The applicable method depends on your personal situation and particular dates. To determine which method is relevant, please refer to the following guidance:

If you are a beneficiary of a retirement or total disability pension, the date that you became a beneficiary corresponds to your pension start date.

If you are a beneficiary of a surviving spouse’s pension or an orphan’s pension, the relevant date is the date when the deceased beneficiary became a beneficiary.

If you are a beneficiary of a retirement pension having participated in the Progressive Retirement Program (PRP), the date you became a beneficiary corresponds to your PRP start date.

If you are a beneficiary of a surviving spouse’s pension or an orphan’s pension following the death of a member, the relevant date is your pension start date.

Should your date be:

on or before 31 December 2011, the applicable method would be I. 1. of Annex C.

between 1 January 2012 and 31 July 2019, the applicable method would be I. 2. of Annex C.

on or after 1 August 2019, the applicable method would be I. 3. of Annex C.

Annex C – Method for the Annual Adjustment of Pension (Article II 1.14)

Definitions

PPL: purchasing power loss.

PPL Account: individual accumulated loss of purchasing power account maintained for each beneficiary, the balance of which shall not exceed 8%.

Geneva CVI: annual variation of the Geneva consumer price index for the last twelve-month period (August to August), expressed in percentage points.

Funding ratio: actual funding ratio of the Fund in a closed fund technical balance sheet as confirmed in the annual financial statements of the Fund approved by the Council.

I. Method for the Annual Adjustment of Pensions

The method applicable for the annual adjustment of pensions differs pursuant to the date on which a person becomes a beneficiary of a pension.

1. Method for the annual adjustment of pensions for persons who became beneficiary of a pension on or before 31 December 2011

a) Persons who became beneficiary of a pension on or before 31 December 2011 shall receive no annual adjustment of pension unless their PPL account maintains a balance of 8%. Provided their PPL account has such a balance, the method set out in paragraphs 1 (b) and (c) shall apply.

b) (i) If the Geneva CVI is positive, the annual adjustment shall be the Geneva CVI, unless the conditions of 1 (c) are fulfilled;

(ii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iii) If the Geneva CVI is negative, no annual adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

2. Method for the annual adjustment of pensions for persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019

a) Persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019, inclusive, shall receive no annual adjustment of pension unless their PPL account maintains no less than the minimum balance set out in Table 1. Provided their PPL account has such a balance, the method set out in paragraphs 2 (b) and (c) shall apply.

b) (i) If the Geneva CVI is positive and the funding ratio is less than 100%, the adjustment shall be the product of the Geneva CVI multiplied by the funding ratio, up to a maximum of the actuarial parameter for annual inflation as set out in the Actuary’s triennial report, always provided that no PPL account may exceed a balance of 8%1 ;

(ii) If the Geneva CVI is positive and the funding ratio is equal to or greater than 100%, the annual adjustment shall be the Geneva CVI, unless the conditions of 2 (c) are fulfilled;

(iii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iv) If the Geneva CVI is negative, no annual adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

3. Method for the annual adjustment of pensions for persons who become beneficiary of a pension on or after 1 August 2019

a) Persons who become beneficiary of a pension on or after 1 August 2019 shall be granted an annual adjustment in accordance with the method set out in paragraphs 3 (b) and (c).

b) (i) If the Geneva CVI is positive and the funding ratio is less than 100%, the adjustment shall be the product of the Geneva CVI multiplied by the funding ratio, up to a maximum of the actuarial parameter for annual inflation as set out in the Actuary’s triennial report, always provided that no PPL account may exceed a balance of 8%2 ;

(ii) If the Geneva CVI is positive and the funding ratio is equal to or greater than 100%, the annual adjustment shall be the Geneva CVI, unless the conditions of 3 (c) are fulfilled;

(iii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iv) If the Geneva CVI is negative, no adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

II. Method for the Annual Adjustment of the Fixed Sum and Allowances

The fixed sum and allowances shall be adjusted annually in accordance with the applicable method for the annual adjustment of pensions as set out above.

1 If a beneficiary’s PPL account maintains a balance of 8% and the Geneva CVI is positive, the Geneva CVI shall be granted notwithstanding the funding ratio of the Fund.

2 If a beneficiary’s PPL account maintains a balance of 8% and the Geneva CVI is positive, the Geneva CVI shall be granted notwithstanding the funding ratio of the Fund.

How do I know what my current purchasing power loss (PPL) balance is?

Every year in December you receive a letter from the Fund with information on the annual adjustment to your benefits effective 1 January the following year. The letter includes your updated purchasing power loss (PPL) balance for the coming year.

Which funding ratio is used in the annual adjustment calculation?

The funding ratio used in the annual adjustment calculation is the funding ratio on an accounting basis and is included in the Statement of Financial Position of the Pension Fund’s last audited Financial Statements.

Which Geneva Cost of living (CVI) is used in the annual adjustment calculation?

The Geneva CVI used in the annual adjustment calculation is Geneva CVI for the last twelve-month period from August to August.

My adjustment calculation depends on the actuarial parameter for annual inflation but where can I find this?

The actuarial parameter for annual inflation, from the last periodic actuarial review, is noted in the actuarial section of the Fund’s Annual Report.

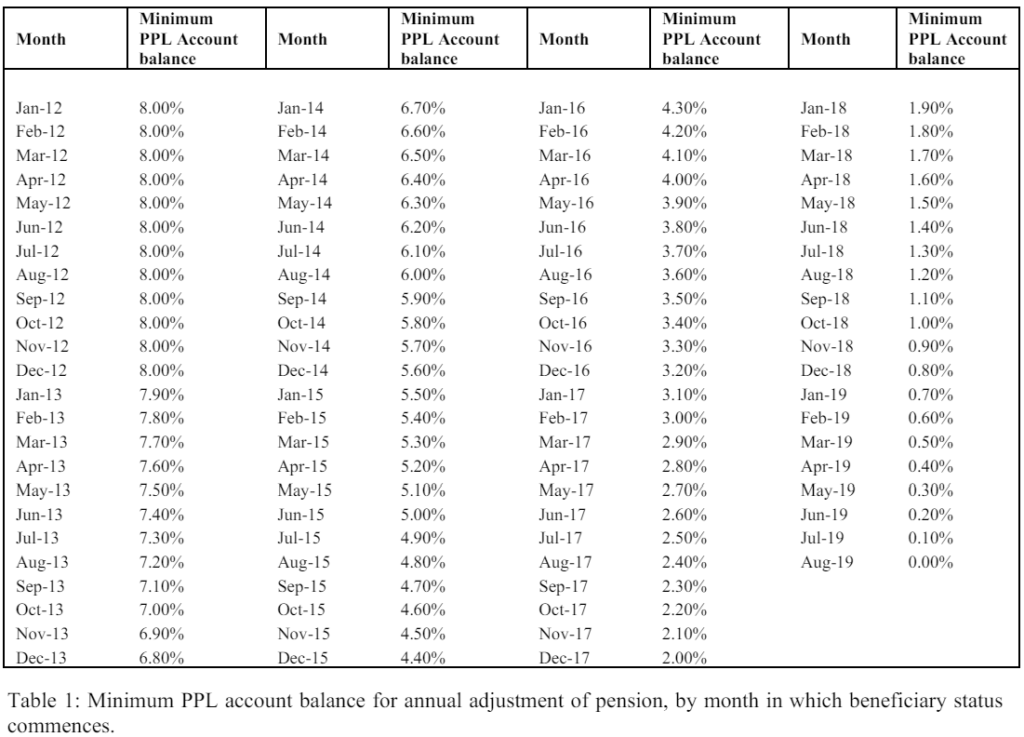

If it is relevant to my situation, what is my minimum PPL account balance?

If, between 1 January 2012 and 31 July 2019:

You became a beneficiary,

You are a surviving spouse or orphan of a deceased beneficiary who became a beneficiary of a pension,

You entered into the Progressive Retirement Program (PRP), or

You are a surviving spouse or orphan of a member who passed away,

You have a minimum PPL account balance. It is based on the month and year of one of the above situations. Your minimum PPL account balance is used to determine whether you will receive an annual adjustment. You will not receive an annual adjustment unless your individual accumulated PPL balance has reached your minimum PPL account balance. The different minimum PPL account balances are set out in Table 1 of Annex C of the Rules and Regulations.

Table 1 – Annex C: Method for the Annual Adjustment of Pension (Article II 1.14)

2. Method for the annual adjustment of pensions for persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019

a) Persons who become beneficiary of a pension between 1 January 2012 and 31 July 2019, inclusive, shall receive no annual adjustment of pension unless their PPL account maintains no less than the minimum balance set out in Table 1. Provided their PPL account has such a balance, the method set out in paragraphs 2 (b) and (c) shall apply.

b) (i) If the Geneva CVI is positive and the funding ratio is less than 100%, the adjustment shall be the product of the Geneva CVI multiplied by the funding ratio, up to a maximum of the actuarial parameter for annual inflation as set out in the Actuary’s triennial report, always provided that no PPL account may exceed a balance of 8%1 ;

(ii) If the Geneva CVI is positive and the funding ratio is equal to or greater than 100%, the annual adjustment shall be the Geneva CVI, unless the conditions of 2 (c) are fulfilled;

(iii) If the Geneva CVI is zero, no annual adjustment shall be granted;

(iv) If the Geneva CVI is negative, no annual adjustment shall be granted but the resulting effective increase in purchasing power shall reduce the balance of the beneficiary’s PPL account.

c) When the funding ratio of the Fund has been greater than 110% for three consecutive years, beneficiaries who have incurred an individual accumulated loss of purchasing power shall be compensated as follows: provided that the Geneva CVI is positive and the funding ratio remains greater than 110%, their annual adjustment of pensions shall be the product of the Geneva CVI multiplied by the funding ratio, until such time as the balance of their PPL account is reduced to zero.

1 If a beneficiary’s PPL account maintains a balance of 8% and the Geneva CVI is positive, the Geneva CVI shall be granted notwithstanding the funding ratio of the Fund.

Why am I not receiving an annual adjustment?

As a beneficiary you have an individual PPL account. This is the individual account maintained for each beneficiary with the accumulated loss of purchasing power i.e. the difference between Geneva CVI and your annual adjustments. Your individual accumulated PPL balance has not reached 8% or your minimum PPL balance so no adjustment is granted.

What happens if Geneva CVI is zero?

If Geneva CVI is zero then you will not receive an annual adjustment.

What happens if Geneva CVI is negative?

If Geneva CVI is negative then you will not receive an annual adjustment, however your PPL account balance will be reduced accordingly, and your benefits will remain unchanged.